Best Business Loans for Boutique Owners in NYC: 5 Funding Options for 2026

Running a boutique in Brooklyn or Manhattan means managing inventory cycles, seasonal rushes, and rising commercial rents, all at the same time. When you need capital to restock, renovate, or simply bridge a slow month, business loans for boutique owners in NYC can make all the difference.

The good news is that alternative lenders today offer faster, more flexible options than traditional banks, and many require no collateral at all. In this guide, you’ll find the five best funding options for NYC boutique owners in 2026, along with the honest pros, cons, and qualification requirements for each.

Why NYC Boutique Owners Struggle with Traditional Bank Loans

New York City is home to more than 183,000 small businesses, and independent boutiques represent a significant share of that number. Brooklyn alone has roughly 46,300 registered small firms, while Manhattan holds approximately 37,500, and retail boutiques are woven throughout both boroughs. Yet, despite their presence and cultural importance, many boutique owners find the traditional banking system frustratingly out of reach.

Banks typically require two or more years of profitability, strong personal credit scores (usually 680+), detailed financial statements, and collateral.

For a boutique owner navigating seasonal swings and thin retail margins, these requirements are often impossible to meet.

Furthermore, the application process at most banks can take 30 to 90 days, far too slow when you need to pay for a shipment arriving next week.

Additionally, alternative business lending has grown significantly to fill this gap. According to Federal Reserve Small Business data, small commercial loans under $1 million grew to $421 billion in Q2 2025 — a clear signal that non-bank lenders are filling the void. The result is a growing ecosystem of funding products designed specifically for businesses like yours.

The 5 Best Funding Options for Brooklyn & Manhattan Boutiques

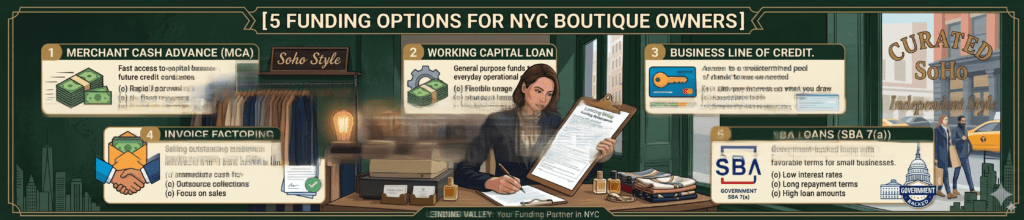

1. Merchant Cash Advance (MCA)

A Merchant Cash Advance is one of the most popular funding tools for boutique retailers in New York City — and for good reason. Instead of a fixed monthly payment, you repay the advance as a small percentage of your daily credit card sales. This means your repayment naturally slows down during your off-season and picks up when sales are strong.

For example, a Williamsburg boutique owner might receive $60,000 upfront. Then, each day, 12% of card sales goes toward repayment — so a $3,000 day means $360 comes back automatically. Consequently, there are no rigid payment schedules, no surprise bills, and no stress during a slow January.

Best for: Boutique owners with steady card volume who need capital fast.

Typical range: $5,000–$500,000

Speed: 24–48 hours from approval to funding

Credit requirement: As low as 500

2. Working Capital Loan

A working capital loan is a short-term, unsecured loan designed to cover everyday operational expenses. Moreover, it’s a strong fit for boutique owners facing seasonal inventory gaps, a surprise rent increase, or an opportunity to buy wholesale merchandise at a discount.

Unlike an MCA, working capital loans carry fixed repayment schedules — typically daily or weekly — over 3 to 18 months. However, they often come with lower total costs than an MCA for borrowers with solid revenue history. Approval is based primarily on your bank deposits and time in business rather than your credit score.

Best for: Boutique owners with consistent monthly revenue who want predictable repayment.

Typical range: $10,000–$500,000

Speed: 24–48 hours

Minimum revenue: ~$10,000/month

3. Business Line of Credit

A business line of credit works similarly to a credit card, you draw funds as needed, up to your approved limit, and only pay interest on what you actually use. This makes it an incredibly flexible tool for boutique owners who want a financial safety net without committing to a lump sum.

In practice, you might draw $20,000 to purchase a new spring collection, repay it over three months, and then draw again for a summer pop-up event.

Furthermore, once you repay a draw, the full credit line is typically restored and available again. For boutique owners in Manhattan who deal with high-volume but unpredictable sales cycles, this revolving access to capital is particularly valuable.

Best for: Boutique owners who need ongoing, flexible access to working capital.

Typical range: $10,000–$250,000

Speed: 1–3 business days for setup; instant draws thereafter

4. Invoice Factoring

While most boutiques sell direct-to-consumer, some NYC boutique owners also supply goods to hotels, corporate clients, event planners, or wholesale buyers — and often wait 30–90 days for payment. Invoice factoring solves this problem by letting you sell those outstanding invoices to a factoring company at 80–90% of their face value, receiving cash immediately.

This option is especially relevant for boutique owners expanding into wholesale or B2B channels. As a result, you don’t have to wait weeks for a hotel spa boutique partner or a corporate gifting client to pay. Instead, you get the cash now and continue investing in your inventory and operations.

Best for: Boutiques with wholesale or B2B customers and outstanding invoices.

Advance rate: 80–90% of invoice face value

Speed: Same day to 24 hours

5. SBA Loans

SBA loans are government-backed loans administered through banks and credit unions, designed to help small businesses access lower interest rates and longer repayment terms than conventional commercial loans. The most common option, the SBA 7(a) loan, offers up to $5 million with terms up to 10 years for working capital.

However, SBA loans come with the most demanding qualification requirements. In addition to a credit score of 680+ and at least two years in business, you’ll typically need tax returns, financial projections, and a detailed business plan. The process can take 30–90 days — so SBA funding is best suited for boutique owners planning ahead, not those facing an immediate cash need.

That said, the SBA Metro New York District actively supports small businesses in the five boroughs, and competitive interest rates (typically 6–9%) make SBA loans worth pursuing for those who qualify.

Best for: Established boutiques planning a major expansion or lease build-out.

Typical range: $50,000–$5,000,000

Speed: 30–90 days

Credit requirement: 680+

Quick Comparison: Side-by-Side Breakdown

Below is a clear, at-a-glance comparison of all five funding options for NYC boutique owners. Use this table to quickly identify which product aligns best with your timeline, revenue, and goals.

| Funding Type | Best For | Amount Range | Speed | Min. Credit Score | Collateral Required? |

|---|---|---|---|---|---|

| Merchant Cash Advance | Card-heavy boutiques needing speed | $5K–$500K | 24–48 hrs | 500 | No |

| Working Capital Loan | Stable revenue, predictable repayment | $10K–$500K | 24–48 hrs | 550 | No |

| Business Line of Credit | Ongoing flexible capital access | $10K–$250K | 1–3 days | 580 | No |

| Invoice Factoring | Boutiques with B2B/wholesale clients | 80–90% of invoices | Same day | N/A (invoice-based) | No |

| SBA Loan | Expansion, long-term growth plans | $50K–$5M | 30–90 days | 680 | Sometimes |

How to Qualify for a Boutique Business Loan in NYC

Qualifying for a small business loan as a boutique owner in New York is significantly more accessible than most owners realize — especially through alternative lenders. While every lender has its own criteria, most alternative funding providers look at a core set of factors.

Minimum Requirements (Alternative Lenders)

To qualify for an MCA or working capital loan, you typically need at least three to six months in business and $8,000–$10,000 or more in monthly bank deposits. Furthermore, lenders will ask for three to six months of business bank statements — no tax returns or P&L statements required for most products. Even if your personal credit score is below 600, you may still qualify as long as your business revenue is consistent.

Documents You’ll Need

The application process is straightforward. Most alternative lenders require just a one-page application, three to six months of business bank statements, and a valid government-issued ID. In some cases, they may also request a voided business check. Notably, the entire process can often be completed online in under 10 minutes.

A Note on the NYC Future Fund

In 2026, Mayor Mamdani launched the $80M NYC Future Fund, a city-backed loan program offering as little as $25,000 at 7.5% interest for qualifying small businesses. This program specifically targets minority-, immigrant-, and women-owned businesses — including boutique owners in underserved Brooklyn and Manhattan neighborhoods. Therefore, if you meet the eligibility criteria, it’s worth exploring alongside private lending options.

Real-World Scenarios: Which Option Fits Your Situation?

Every boutique is different. To help you apply these options practically, here are three scenarios that reflect common situations NYC boutique owners face.

Scenario A: Pre-Season Inventory Crunch (Brooklyn Boutique)

A boutique owner in Williamsburg has a major wholesale order arriving in three weeks — but cash is tied up in last season’s slow-moving inventory. She needs $35,000 quickly to cover the order. In this case, a Merchant Cash Advance is her best option. She can apply today, get approved tomorrow, and have funds in her account within 48 hours. Repayment happens automatically as a percentage of daily card sales, so she doesn’t need to worry about fixed monthly obligations during the post-season lull.

Scenario B: Store Renovation (Manhattan Boutique)

A boutique on the Upper East Side is relocating to a larger space with a 60-day build-out timeline. The owner has excellent revenue and two years in business but needs $120,000 for renovation costs and new fixtures. A working capital loan is the right fit here. He can lock in a fixed repayment schedule, plan his budget accordingly, and have the full amount funded within two days of approval — well ahead of the contractor start date.

Scenario C: Wholesale Expansion (Multi-Channel Boutique)

A boutique in Fort Greene sells direct-to-consumer in-store but has recently begun supplying corporate gifting clients. Her clients are on net-60 payment terms, meaning she often waits two months for $40,000+ in outstanding invoices. Invoice factoring transforms those receivables into immediate cash, allowing her to restock for her retail floor while waiting for the B2B payments to clear. Consequently, her cash flow stays healthy on both channels simultaneously.

Ready to Get Funded? It Takes Less Than 10 Minutes.

Lending Valley has helped hundreds of NYC boutique owners secure fast, flexible funding — with approvals in as little as 24 hours and no collateral required. Whether you need $10,000 or $500,000, we’ll match you with the right product for your business.

Frequently Asked Questions

What is the easiest business loan for boutique owners in NYC to qualify for?

A Merchant Cash Advance (MCA) is typically the easiest option for NYC boutique owners. Lenders focus on your monthly card sales rather than credit score, and approvals can happen in as little as 4–24 hours with funding the same or next day. Moreover, the application is simple and doesn’t require tax returns or collateral.

How much can a boutique owner in Brooklyn or Manhattan borrow?

Most alternative lenders offer between $5,000 and $500,000 for retail boutique owners. The exact amount depends on your monthly revenue, time in business, and the funding product you choose. Generally, lenders will advance between 75% and 150% of your average monthly revenue.

Do I need collateral to get a business loan for my boutique?

No. Merchant cash advances, working capital loans, and business lines of credit from alternative lenders are typically unsecured — meaning no collateral is required. Your revenue and business performance are the primary qualifiers. SBA loans, however, may require collateral for larger amounts.

Can I get a boutique business loan with bad credit?

Yes. Alternative lenders like Lending Valley approve boutique owners with credit scores as low as 500. They prioritize your monthly bank deposits and time in business over your personal FICO score. As a result, even owners with past credit challenges are often approved when their business generates consistent revenue.

How fast can a NYC boutique owner get funded?

With an MCA or working capital loan from an alternative lender, you can receive funds in as little as 24–48 hours after approval. In contrast, traditional bank loans can take 30–90 days or more, making them a poor fit for urgent capital needs. For the fastest funding, alternative lenders are the clear choice.

The Bottom Line

NYC boutique owners in Brooklyn and Manhattan face real challenges, seasonal cash flow gaps, rising rents, competitive inventory demands, and a banking system that was never designed for fast-moving retail. The good news is that business loans for boutique owners in NYC have never been more accessible.

Whether you need a fast Merchant Cash Advance to cover an inventory order, a working capital loan for a renovation, or a flexible line of credit for ongoing needs, alternative lenders can fund you in as little as 24–48 hours with no collateral required.

Additionally, the new NYC Future Fund offers city-backed financing at competitive rates for qualifying minority-, immigrant-, and women-owned boutiques. Furthermore, if you’re planning long-term expansion, SBA loans remain the gold standard for low-rate, long-term capital.

Above all, the worst move is waiting too long and missing a growth opportunity because capital wasn’t in place.

Apply with Lending Valley today, it takes less than 10 minutes, and you could have an offer within 24 hours.

For more resources on small business loans, bad credit business funding, and finding the right funding provider, explore Lending Valley’s full guide library.

Sources: SBA Metro New York District | Federal Reserve Small Business 2025 Chartbooks | NYC Mayor’s Office — NYC Future Fund 2026