Running a small business is exciting, but it can also be tough when it comes to managing finances. Whether it’s paying staff, purchasing equipment, or replenishing inventory, businesses often require quick access to cash.

Large corporations can raise billions through banks or investors, but small businesses usually face steep challenges. This is where merchant cash advances (MCAs) came in as a new solution.

In the dynamic world of business financing, the merchant cash advance (MCA) has emerged as a compelling solution for many entrepreneurs.

But what exactly is a merchant cash advance company, and how does it operate? This article aims to unravel the complexities of MCAs, demystifying this often-misunderstood funding option. Unlike traditional loans, merchant cash advances provide quick capital based on future sales, offering flexibility when cash flow is tight.

Through a blend of insightful real-life examples and thorough explanations, we’ll explore how these companies assess risk, determine advances, and seamlessly integrate with the needs of businesses.

If you’ve ever wondered how you can swiftly access funds without the burdensome paperwork, keep reading to unlock the mystery behind merchant cash advances and discover if this financing method is the right fit for you.

What is a Merchant Cash Advance Company?

Merchant cash advance companies are financial institutions that provide businesses with quick access to capital in exchange for a portion of future sales. Unlike traditional lending institutions, these companies don’t offer loans but instead advance money based on the anticipated revenue of a business.

This alternative financing method can be particularly useful for businesses that need immediate funds and may not qualify for conventional loans due to stringent credit requirements or lengthy approval processes.

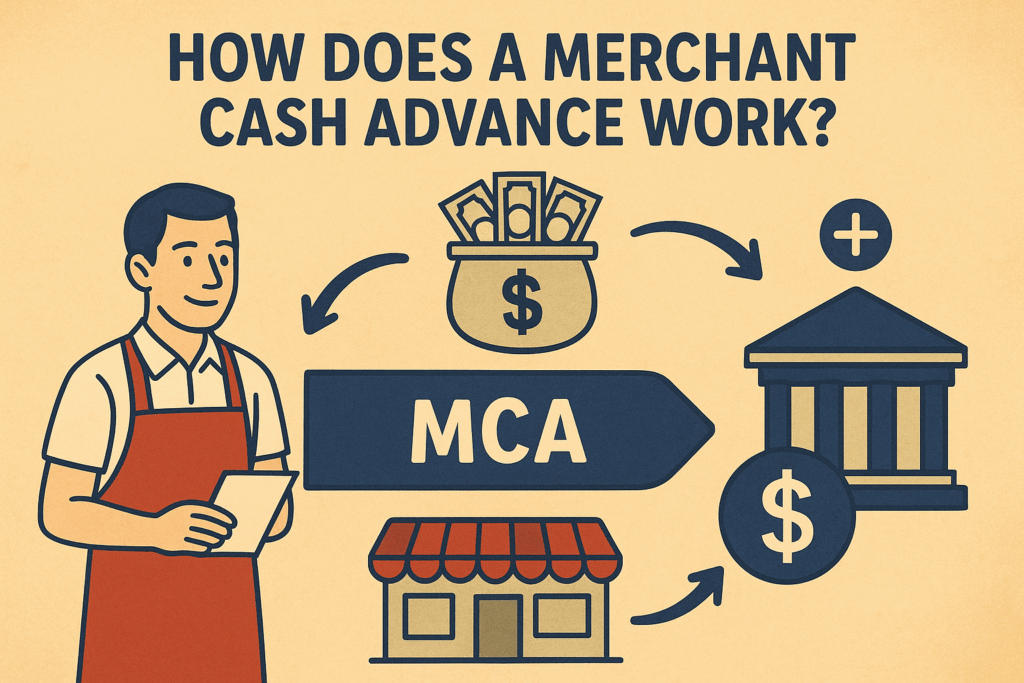

The core mechanism of a merchant cash advance (MCA) involves purchasing future sales at a discount.

Essentially, an MCA company provides a lump sum to the business upfront. And the business agrees to repay this amount by allowing the MCA company to take a fixed percentage of its daily sales until the advance is paid off.

This percentage is typically deducted from credit card transactions or bank deposits, making repayment relatively seamless and aligned with the business’s cash flow.

Merchant cash advance companies are often seen as a lifeline for small businesses, retail stores, restaurants, and other enterprises that experience fluctuating revenues.

The flexibility of repayment terms and the speed at which funds can be accessed make MCAs an attractive option for addressing urgent financial needs, such as covering payroll, purchasing inventory, or handling unexpected expenses.

However, understanding the intricacies of how these companies operate and the implications of opting for an MCA is crucial for making informed financial decisions.

How Merchant Cash Advances Work

Merchant cash advances work by providing businesses with a lump sum of cash in exchange for a percentage of future sales.

The process begins with the business owner applying for an MCA, where they typically need to provide information about their business’s sales history, revenue, and other financial details.

Unlike traditional loan applications, the paperwork involved in applying for an MCA is minimal, and the approval process is often swift, sometimes taking just a few days.

Once approved, the MCA company will offer an advance amount based on the business’s projected sales. This advance amount is calculated by assessing the business’s average monthly revenue and other risk factors.

The company then determines a retrieval rate, which is the percentage of daily sales that will be used to repay the advance.

For example, if a business receives a $50,000 advance with a retrieval rate of 10%, the MCA company will collect 10% of the business’s daily credit card sales until the advance is repaid.

Repayment is typically automated, with the agreed-upon percentage deducted directly from the business’s credit card transactions or bank deposits. This structure ensures that repayment amounts fluctuate with the business’s sales volume, offering flexibility during slower periods. However, it also means that repayment can be faster during peak sales times.

The convenience and speed of MCAs make them a popular choice for businesses needing immediate capital without the rigors of traditional loan applications.

Big Companies vs. Small Businesses: Why Funding Differs

The report starts by showing how big and small companies raise money differently:

- Large corporations can issue bonds or shares worth billions. They have auditors, lawyers, analysts, and investors all reviewing them. Because of their size, the cost of raising money is low compared to the amount they raise.

- Small businesses, on the other hand, struggle. Banks ask for collateral, years of financial records, and personal guarantees. Equity investors often want a big chunk of ownership. This makes raising money either very expensive or nearly impossible.

This problem is called the “size challenge”, small deals are costlier (in percentage terms) because professional fees and requirements don’t shrink enough for small businesses to manage.

How Merchant Cash Advances Work

Merchant cash advances were created to fill this funding gap using technology.

- A business sells a portion of its future sales to a lender at a discount.

- Example: A restaurant gets $60,000 now in exchange for repaying $80,000 from future card sales.

- Repayment happens automatically: every day, a fixed % (say 8%) of debit and credit card sales is “swept” into the lender’s account.

This is similar to factoring (selling unpaid invoices), but instead of past receivables, MCAs are based on future sales.

Why MCAs Appeal to Small Businesses

The report highlights several advantages:

- Quick and Simple – Approval is based on recent sales data, not years of financial history or collateral.

- No Equity Loss – Business owners don’t have to give up ownership.

- Technology Makes It Easy – Automated payments keep collection costs low.

- Comparable Costs – While MCAs can look more expensive than bank loans, they often skip the hefty legal and banking fees that small loans usually carry.

Read more about Female Small Business Loans

A Brief History of MCAs

- The industry started in the late 1990s in the U.S., led by AdvanceMe Inc.

- More players entered, leading to a lawsuit over patents. By 2007, courts ruled that the idea wasn’t unique, opening the market to competition.

- In Canada, MCAs only emerged in 2006, with companies like AdvanceIt and Merchant Advance Capital.

- Since then, MCAs have spread widely as an alternative financing tool.

Public Policy and Economic Impact

Small businesses are crucial; they create nearly 60% of jobs in Canada and drive economic growth. Yet traditional programs like the Canadian Small Business Financing Program often burden entrepreneurs with paperwork and strict requirements.

MCAs step in to provide fast, accessible capital, which can help businesses grow and hire more people. The report suggests that innovation like MCAs supports job creation and strengthens the economy.

Key Differences Between Merchant Cash Advances and Traditional Loans

One of the most significant differences between merchant cash advances and traditional loans is the method of repayment. Traditional loans require fixed monthly payments, regardless of the business’s revenue fluctuations.

In contrast, MCAs align repayment with the business’s sales performance, deducting a percentage of daily transactions.

This variable repayment structure can be beneficial during slow sales periods, as businesses aren’t burdened with high fixed payments.

Another key distinction lies in the approval process. Traditional loans often have stringent requirements, including high credit scores, extensive documentation, and long approval times.

MCA companies, however, focus more on the business’s sales history and future revenue potential. This results in quicker approvals and fewer barriers for businesses that may not meet the criteria for conventional loans.

The simplified application process is a significant advantage for many small business owners.

Furthermore, the cost structure of MCAs differs from traditional loans. While loans typically have interest rates and fees, MCAs use a factor rate to determine the total repayment amount. A factor rate is a multiplier applied to the advance amount, which can result in higher overall costs compared to traditional loans.

For example, an MCA with a factor rate of 1.3 on a $50,000 advance means the business will repay $65,000. Understanding these differences is crucial for businesses to evaluate the true cost and suitability of an MCA versus a traditional loan.

Advantages of Using a Merchant Cash Advance

One of the primary advantages of using a merchant cash advance is the speed of funding. Businesses can often receive funds within days, which is invaluable when facing urgent financial needs.

This fast access to capital can help businesses seize opportunities, manage cash flow gaps, or handle unexpected expenses without the delays associated with traditional loans.

Repayment flexibility is another significant benefit. Since MCAs are repaid through a percentage of daily sales, businesses don’t have to worry about fixed monthly payments.

This can be particularly advantageous during periods of fluctuating revenue. When sales are slow, the repayment amount decreases, easing the financial burden. Conversely, during high sales periods, repayments are higher, potentially allowing the advance to be repaid more quickly.

Additionally, the streamlined application process and lower approval barriers make MCAs accessible to a wider range of businesses.

Companies with lower credit scores or limited credit history may find it challenging to secure traditional loans. MCA companies prioritize sales performance and future revenue, making it easier for businesses to qualify for funding.

This inclusivity helps many small businesses and startups access the capital they need to grow and succeed.

Potential Risks and Drawbacks of Working with a Merchant Cash Advance Company

Despite the advantages, merchant cash advances come with potential risks and drawbacks that businesses must carefully consider.

One of the primary concerns is the cost. The factor rates used in MCAs can result in higher overall repayment amounts compared to traditional loans.

This can make MCAs an expensive financing option, particularly if the business’s sales don’t grow as anticipated.

Another risk is the impact on cash flow. Since repayments are tied to daily sales, a significant portion of revenue is continually directed towards repaying the advance. This can strain the business’s cash flow, especially if sales decline unexpectedly.

Businesses must ensure they can manage their cash flow effectively while meeting the repayment obligations of an MCA.

Additionally, the lack of regulatory oversight in the MCA industry can pose risks. Unlike traditional lending institutions, MCA companies are not subject to the same regulations, which can lead to varying practices and potential for predatory lending.

Businesses must conduct thorough research and due diligence before choosing an MCA provider to avoid falling victim to unfavorable terms or unethical practices.

Real-Life Examples of Merchant Cash Advances in Action

To better understand how merchant cash advances work in real-life scenarios, let’s explore a few examples.

Consider a small restaurant experiencing a sudden surge in demand during the holiday season. The owner needs to purchase additional inventory and hire temporary staff to meet the increased customer flow. Instead of applying for a traditional loan, which may take weeks for approval, the owner opts for an MCA. Within days, they receive the funds needed to stock up on supplies and manage the holiday rush.

Another example involves a retail store facing unexpected repairs due to a burst pipe. The store owner requires immediate capital to fix the damage and prevent further losses.

Given the urgency, the owner turns to an MCA company and quickly secures the necessary funds. The repayment is made through daily credit card sales, allowing the store to recover without the pressure of large monthly payments.

A third example is a tech startup that has developed a new product but lacks the funds for marketing and distribution.

Recognizing the potential for high sales, the startup applies for an MCA. With the advance, they launch an aggressive marketing campaign and successfully introduce the product to the market. The flexible repayment structure aligns with their sales growth, ensuring manageable repayments while boosting their business.

Who Should Consider a Merchant Cash Advance?

Merchant cash advances can be a suitable option for various types of businesses facing specific financial needs. Small businesses, such as retail stores, restaurants, and service providers, often benefit from the quick access to capital that MCAs offer.

These businesses frequently experience fluctuating revenue and may need immediate funds to address seasonal demands, unexpected expenses, or growth opportunities.

Startups and young companies with limited credit history may also find MCAs appealing. Traditional loans often require extensive credit checks and established credit scores, which can be a barrier for new businesses.

MCAs focus more on future sales potential, making it easier for startups to qualify for funding. This can provide the necessary boost to get the business off the ground or expand its operations.

Businesses experiencing temporary cash flow issues can also consider MCAs. Whether due to delayed receivables, unexpected costs, or seasonal fluctuations, MCAs provide a fast solution to bridge financial gaps.

The repayment flexibility ensures that businesses aren’t overwhelmed by fixed monthly payments, offering a more manageable approach to addressing short-term financial challenges.

Tips for Choosing the Right Merchant Cash Advance Company

Selecting the right merchant cash advance company is crucial for ensuring favorable terms and avoiding potential pitfalls.

First and foremost, businesses should thoroughly research and compare different MCA providers. Look for companies with transparent terms, competitive interest rates, and positive customer reviews. Transparency is key to understanding the true cost and repayment structure of the advance.

It’s also essential to assess the company’s reputation and track record. Established MCA providers with a history of satisfied customers are more likely to offer reliable and ethical services.

Check for any complaints or legal issues that may indicate predatory practices. A reputable company should be willing to provide clear explanations and answer any questions regarding their terms.

Businesses should also consider the flexibility of repayment options. Some MCA companies offer customizable retrieval rates or seasonal adjustment plans, which can be beneficial for businesses with fluctuating revenues.

Ensure that the repayment structure aligns with your sales patterns and cash flow requirements. Additionally, inquire about any fees or penalties for early repayment to avoid unexpected costs.

Conclusion and Final Thoughts

Merchant cash advances offer a unique and flexible financing solution for businesses in need of quick capital. By providing funds based on future sales, MCA companies enable businesses to address immediate financial needs without the burdens of traditional loans.

The speed of funding, flexible repayment terms, and accessibility make MCAs an attractive option for small businesses, startups, and companies facing temporary cash flow challenges.

However, it’s essential to weigh the potential risks and drawbacks, including the higher costs and impact on cash flow.

Thorough research, due diligence, and careful consideration are crucial for selecting the right MCA provider and ensuring favorable terms.

Real-life examples demonstrate the practical applications of MCAs, highlighting their benefits in various scenarios.

Ultimately, merchant cash advances can be a valuable financial tool when used wisely. By understanding how they work and assessing their suitability for your business, you can unlock the mystery behind MCAs and make informed decisions to support your business’s growth and success.

Whether facing urgent expenses or seeking expansion opportunities, MCAs offer a viable path to accessing the capital you need.