Close

You have delivered the product. You have sent the invoice. Now, you sit and wait.

If you are a business owner, you know the visceral pain of “Net-60” or “Net-90” terms. On paper, you are rich. Your Profit & Loss statement shows a killer month with record-breaking revenue. But in your bank account? Crickets. You can’t pay payroll with a PDF invoice, and you certainly can’t buy inventory with an “IOU” from a client.

This is the cash flow gap that kills perfectly healthy businesses.

In 2026, the solution isn’t to nag your clients for early payment (and risk looking desperate). The solution is account receivable loans. It is the financial tool that lets you unlock the cash trapped in your unpaid invoices immediately.

As a financial advisor watching the market tighten this year, I’ve seen account receivable loans become a lifeline for B2B companies. It’s not about debt; it’s about access. The market for this type of financing is exploding, projected to reach over $182 billion this year alone.

Here is everything you need to know about using your invoices to fund your growth, stripped of the banking jargon.

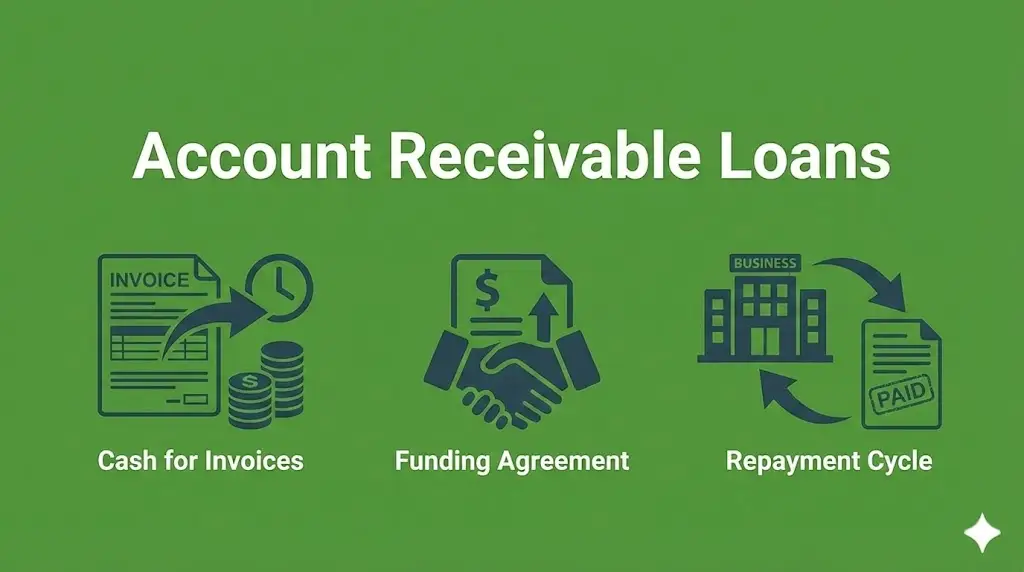

Think of an Account Receivable loan as a line of credit backed by your unpaid invoices.

Unlike a traditional term loan, where the bank looks at your real estate or equipment as collateral, an AR lender looks at who owes you money. If you have invoices due from reputable companies (like Walmart, the City of New York, or a large tech firm), those invoices are tangible assets.

The Simple Mechanism: First, you generate an invoice for work completed let’s say for $100,000. Instead of waiting two months for payment, you submit this invoice to a lender. The lender verifies the invoice and advances you 80-90% of that value ($80k-$90k) immediately, usually within 24 hours. You use that cash to run your business. Later, when your customer finally pays the invoice, the lender sends you the remaining 10-20%, minus a small fee known as the discount rate. It is fast, scalable, and in 2026, it is largely automated.

The lending world has shifted dramatically. Traditional banks have tightened their belts, making standard lines of credit harder to get for small businesses. In fact, data shows that delayed payments are trapping enormous amounts of capital over Rs 8.1 lakh crore in some global markets stifling growth for small enterprises.

In the US, the story is similar. Banks are approving fewer unsecured lines of credit, pushing businesses toward asset-based lending like account receivable loans. The market size is growing at a compound annual growth rate of 11.3%, driven by a rising demand for short-term working capital and the need to bridge the gap between delivery and payment. With AI integration in accounting software now standard, lenders can “plug in” to your books and approve funding in minutes, not weeks.

To understand how this works, let’s look at three specific businesses that used Account receivable loans to survive and scale in different US markets.

A boutique marketing firm in Manhattan landed a massive campaign with a Fortune 500 beverage company. The contract was worth $500,000, but the payment terms were strict: Net-90. The agency faced a critical problem: they needed to hire freelancers and buy media now. They couldn’t wait three months for the cash. So they looked for Business funding in Newyork but were rejected by two banks because their “assets” were just laptops and desks banks didn’t value their intellectual property.

They turned to an Account Receivable loan. The lender verified the contract with the beverage company and advanced $400,000 (80%) on Day 1. The agency executed the campaign flawlessly. When the client paid 90 days later, the lender took their fee and released the rest. This strategy is now a staple for agencies seeking Business funding in Newyork to compete with the giants.

A lumber supplier in Miami was booming with orders flying in. However, they had to pay their timber mills upfront, while their construction clients paid them 60 days after delivery. A huge order came in for a new hotel project. Without cash to buy the wood, they would have to turn down the job. They searched for a Business loan in Florida, but traditional underwriting was taking too long.

They decided to leverage their $200k in outstanding invoices from previous jobs. An AR lender advanced them $160k immediately. They bought the inventory, fulfilled the hotel order, and doubled their quarterly revenue. For construction-adjacent industries, using invoices to secure a Business loan in Florida is often faster and more effective than using real estate collateral because the asset (the invoice) is liquid.

A fast-growing auto parts maker in Cleveland had a steady stream of orders from major car brands. However, a sudden machine breakdown required immediate repair costing $50k. All their cash was tied up in “Works in Progress” and unpaid invoices. They needed Small Business funding in Ohio rapidly to avoid halting the production line.

Instead of taking a high-interest Merchant Cash Advance, they financed their receivables. The lender saw the strength of the invoices from the car brands and funded them within 24 hours. The line was back up in two days. The cost of capital was significantly lower than other options for Small Business funding in Ohio, saving them margin in the long run.

People confuse these two constantly, but the distinction is vital for your control over customer relationships.

Account Receivable Loans (Asset-Based Lending): In this model, you keep the invoice and you borrow against it. Your customer usually doesn’t know the lender exists. You maintain control of the collection process. If you value privacy and client relationships, this is often the preferred route.

Invoice Factoring: Here, you actually sell the invoice to the factor. The factor often takes over the collection process, meaning they call your customer to get paid. This can be intrusive, but it offloads the administrative burden of collections. It is typically more expensive than a loan structure.

The Pros:

The Cons:

You might worry about the fees, but when you compare the cost of financing against the cost of stalled operations, the math often favors speed a concept we explore deeper in Fuel Costs vs. Factoring.

Myth: “Using Account receivable loans means my business is failing.” Fact: Completely false. Major corporations like Amazon and Walmart suppliers use supply chain financing (a form of AR lending) daily. It is a strategic tool for growth, allowing you to shorten your cash conversion cycle and reinvest capital faster.

Myth: “My customers will get harassed by the lender.” Fact: Only if you choose “Notification Factoring.” With a modern AR Loan (or “Non-Notification” financing), the transaction is invisible to your client. They pay you, and you pay the lender.

Myth: “I can finance any invoice.” Fact: No. Lenders usually avoid invoices that are already 90+ days overdue. They want “fresh” receivables that are likely to be paid.

Understanding whether you are borrowing money or selling an asset is critical, a distinction we explore fully in our guide to advances vs loans in USA.

If you are looking for Business funding in Newyork, Small Business funding in Ohio, or anywhere else, you have three main paths.

1. Traditional Banks (Chase, Wells Fargo)

2. Online Fintechs (Bluevine, Fundbox)

3. Lending Valley (The Advisor Approach)

If you want to see how these AR lenders stack up against other top-rated options, check out our deep dive into the Top 3 Business Funding Providers USA with 100+ Trusted Reviews.

At Lending Valley, we see account receivable loans differently. We know that a computer algorithm can’t always see the value of a relationship you have with a client.

We humanize the process. If you are seeking a Business loan in Florida and your credit score took a hit last year because of a hurricane, an algorithm rejects you. We don’t. We look at the quality of your invoices and tell your story to the lender. Our approval rates are high because we operate as a marketplace, matching you with lenders who specialize in your industry whether that’s construction, staffing, or manufacturing.

Real clients confirm this approach works. Reviews from 2025 and 2026 highlight the “legendary status” of advisors like Chad Otar, who help clients navigate complex funding needs when speed is critical. Clients praise the “speed and professionalism” and note that funding often happens in less than a week. If you are tired of hearing “No” because of a rigid bank policy, we are the “Yes” you have been looking for.

Speak to a Lending Valley Advisor, Get matched with the best AR lenders for your industry in minutes.

Whether you choose factoring or a term loan, the key to fast approval is organization, so take a moment to download our checklist of The “Must-Have” Business Funding Documentation.

A: Yes. Since the loan is secured by the invoice, the lender cares more about your customer’s ability to pay than your personal FICO score. This makes it a great option for those who have been denied Small Business funding in Ohio or elsewhere due to credit issues.

A: Generally, yes. Account receivable loans are typically cheaper than MCAs because they are secured by an asset (the invoice). MCAs are based on future sales and carry higher risk premiums.

A: Staffing agencies, trucking/logistics, manufacturing, advertising agencies, and commercial construction are the best fits.

A: No. They usually advance 80-90%. The remaining 10-20% is held in a “reserve account” and released to you (minus fees) once the customer pays the invoice.

A: Rates vary, but typically range from 1% to 3% of the invoice value per month. It is cheaper than a credit card but more expensive than a 10-year bank loan.

A: Yes. This is called “Spot Factoring” or “Single Invoice Financing.” You don’t have to finance your whole book of business if you just need cash for one specific project.

A: Absolutely. New York is a global hub for staffing and ad agencies, two industries that rely heavily on AR financing. Lenders are very active and competitive in the NY market.

Here is the bottom line: When you offer Net-60 terms to a client, you are essentially giving them an interest-free loan. You are acting as their bank.

Stop it.

You are in business to make money, not to finance a Fortune 500 company’s float. Account receivable loans allow you to reclaim control of your cash flow. You get paid for your work today, so you can fund the work for tomorrow.

Whether you are a construction firm needing a Business loan in Florida, a manufacturer looking for Small Business funding in Ohio, or an agency seeking Business funding in Newyork, your invoices are your golden ticket. Don’t let your growth sit in an “Accounts Receivable” folder gathering dust. Unlock it.

Get a Free Invoice Audit Now! See how much capital you can unlock from your current Aging Report.