Running a business is tough. But running one as a minority, woman, or veteran entrepreneur can feel like juggling three jobs at once, managing operations, finding clients, and chasing funding that often feels just out of reach.

The good news? 2025 is a turning point.

More government programs, state-backed initiatives, and mission-driven lenders are finally stepping up to make access to capital faster, fairer, and simpler.

So grab your coffee, and let’s walk through the best financing options available right now, explained in plain English, with real examples and tips that actually matter.

🌎 The 2025 Funding Landscape at a Glance

Before diving into specifics, here’s the reality check:

- The SBA (Small Business Administration) broke records this year, with over 84,000 loans totaling nearly $45 billion going to small businesses. That’s the highest in U.S. history.

- The State Small Business Credit Initiative (SSBCI 2.0) is still rolling out across the country, turning every $1 of state funding into roughly $10 of private lending.

- CDFIs (Community Development Financial Institutions) are thriving, with $8.8 million in fresh federal support to help more local and underserved entrepreneurs access fair loans.

In short: there’s real money out there. You just need to know where to look.

Looking for a rapid and reliable Merchant Cash Advance? Get in touch today! MCA lender

💼 1. SBA 7(a) and 504 Loans — Best for Growth and Stability

If you’re looking for a classic “get it done” business loan, start here.

The SBA 7(a) and 504 programs are perfect for expanding, buying equipment, or refinancing expensive debt.

Why they’re great:

- Long repayment terms (up to 25 years).

- Interest rates that are much lower than short-term online loans.

- Easier approval when backed by the SBA guarantee.

2025 update: The SBA tweaked its fees and guidelines this year. Some veteran-owned or manufacturing businesses can even get fee waivers on certain loans.

🧠 Pro tip: Always ask your lender for the latest FY2025 fee schedule, because a few percentage points can mean thousands saved.

🏛️ 2. SSBCI 2.0 — The “Hidden Gem” State Program

You’ve probably never heard of SSBCI, but you should.

This federal-state partnership helps banks lend to small businesses that might otherwise be declined.

Think of it as a safety net: the state shares the risk with your lender, making approvals easier, especially for minority- or women-owned firms.

How to access it:

Ask your local bank or CDFI, “Are you part of your state’s SSBCI lending network?”

If they say yes, bingo. You’ve just opened a faster path to approval.

🤝 3. CDFIs — The Local Heroes of Community Lending

If you’ve ever felt brushed off by a traditional bank, a CDFI might change that story.

They’re nonprofit or mission-driven lenders built to serve underserved and underestimated founders. They care less about your credit score and more about your story, cash flow, and potential.

Real story (2025):

A small logistics company in South Texas partnered with NeighborWorks Laredo, a newly certified CDFI, to secure affordable financing and business coaching. That one partnership kept 20 local jobs alive.

If you’re rebuilding credit or just starting out, start with a CDFI before you go to a big bank.

💪 4. MBDA — Minority Business Development Agency Support

Here’s a program that deserves more attention.

The MBDA (part of the U.S. Department of Commerce) runs business centers nationwide that help minority founders become lender-ready, from refining their financials to finding investors.

In 2025, the MBDA launched $11 million in new funding to train and assist more minority entrepreneurs.

Think of them as your personal “capital coach.”

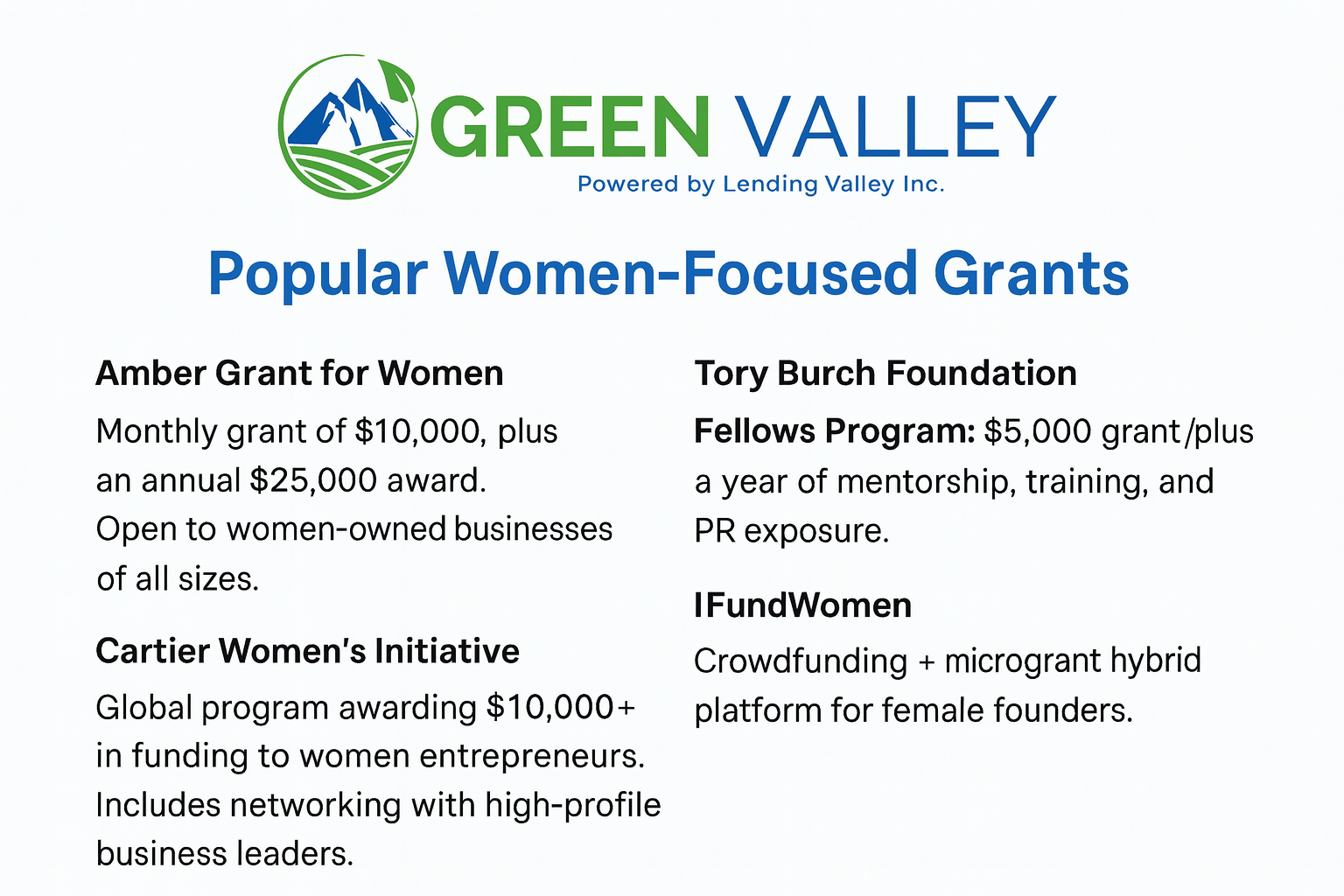

👩💼 5. Women-Owned Business Funding and Grants

Good news, ladies — 2025 has been your year.

- The WOSB (Women-Owned Small Business) certification opens the door to 5% of all federal contracting dollars.

- Private programs like BMO’s Celebrating Women Grant gave out $150,000 to women-led startups across the U.S.

- AT&T’s “She’s Connected” campaign offered cash grants and mentorship, a combo that’s priceless for scaling.

If you haven’t yet, visit the SBA’s WOSB portal and start your certification process. It takes time, but it’s worth every minute.

🎖️ 6. Veteran-Owned Business Funding

Veteran entrepreneurs, you’ve got unique advantages too.

The VetCert program centralizes certification so you can qualify for Service-Disabled or Veteran-Owned Small Business contracts.

Pair that with an SBA Express Loan (which waives certain fees for veterans), and you’ve got one of the fastest approval pipelines available in 2025.

Need help preparing your paperwork?

Reach out to a Veterans Business Outreach Center (VBOC), and they’ll walk you through it for free.

📊 Real 2025 Success Stories

- California Wildfire Relief (Women-Owned):

After the Eaton Fire, 50 women-owned businesses received $25,000 each through a partnership between 11:11 Media Impact and GoFundMe.org, a total of $1.25M in direct aid. - Texas Logistics Company (Minority-Owned):

NeighborWorks Laredo’s CDFI certification unlocked fresh capital for dozens of minority entrepreneurs in border communities. - BMO Women in Business Grant (National):

15 women-led companies each received $10,000 grants to expand their teams and launch new products in 2025.

US TRUST and Lending Valley did a speciality deal together on a syndication basis. Chad is a very wise business owner and real funder.

These stories prove one thing: access to capital is finally starting to shift in the right direction.

🧩 Which Option Fits You Best?

| Business Type / Goal | Start Here | Why |

|---|---|---|

| Need low-cost, long-term capital | SBA 7(a) or 504 Loan | Lowest interest, longest term |

| Struggle with approval odds | SSBCI or CDFI | Easier approvals, more flexible |

| Women-owned startup or scaling brand | WOSB + BMO / AT&T Grants | Free grants + contracts |

| Veteran-owned business | VetCert + SBA Express | Fast approval, fee waivers |

| Minority entrepreneur seeking mentorship | MBDA Business Center | Training + lender intros |

🧠 Smart Tips Before You Apply

- Prep your documents: Banks love organized founders. Keep 3–6 months of statements and a clear business plan ready.

- Leverage your certification: WOSB, VetCert, or Minority-Owned credentials can unlock better loan terms.

- Ask about SSBCI participation: That one question can turn a “maybe” into a “yes.”

- Mix & match: Pair a small grant or SSBCI-backed loan with an SBA loan for sustainable growth.

- Don’t be shy: Local CDFIs want to lend, they just need you to start the conversation.

💬 Final Thoughts

Getting funding in 2025 doesn’t have to feel impossible.

Yes, paperwork, acronyms, and lender jargon can make anyone’s head spin. But today, there are more doors open than ever before for minority-, women-, and veteran-owned businesses.

Start local. Ask questions. And don’t settle for “we’ll get back to you.”

You’ve earned the right to get funded…now go claim it.