Running a food truck or catering business in New York City is equal parts passion and hustle , but it all grinds to a halt without the right capital.

Whether you need to replace a busted generator, stock up for a summer festival, or finance your first commissary kitchen contract, food truck financing in NYC can mean the difference between a missed opportunity and your best quarter yet.

The good news: today’s alternative lenders have made it faster and easier than ever for mobile food operators to access the working capital they need , often in 24 hours or less.

Below, we break down the five most effective funding options for New York City food trucks and caterers, including who each option suits best, what you’ll realistically qualify for, and how quickly you can get funded.

Why NYC Food Trucks Need Specialized Funding

The U.S. food truck industry is booming. According to IBISWorld, the U.S. food truck industry is worth approximately $2.8 billion in 2026, with over 58,000 businesses operating nationwide. In a market as competitive as New York City, staying ahead often requires capital you simply don’t have sitting in a bank account.

NYC food trucks face a unique set of financial pressures that traditional brick-and-mortar restaurants don’t:

- Seasonal cash flow gaps , Revenues spike in summer and drop sharply in winter, creating lulls that strain operating budgets.

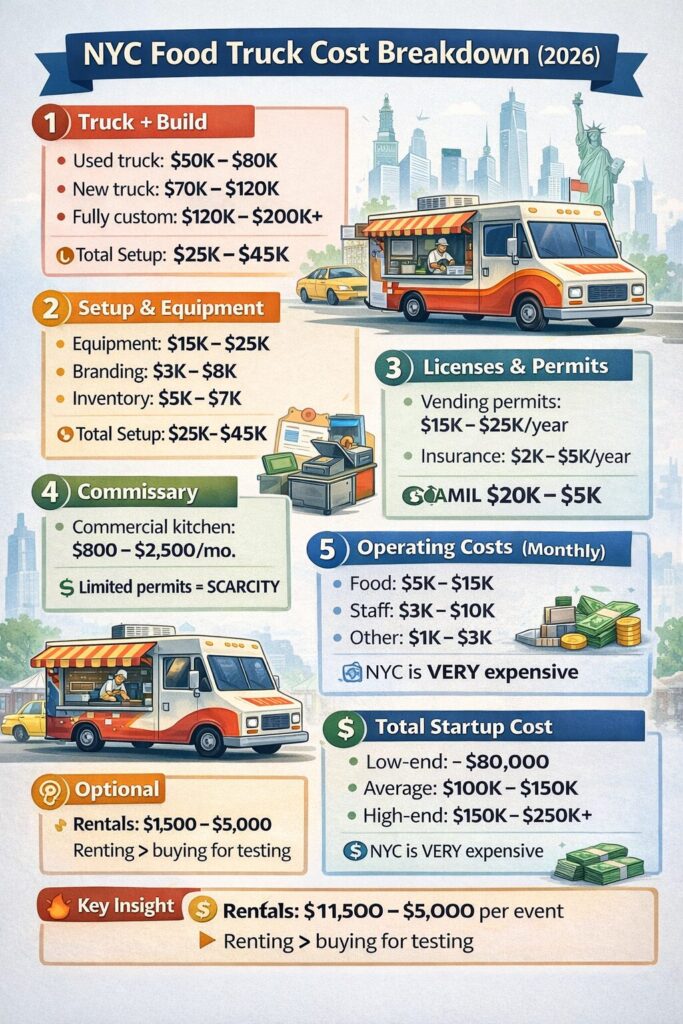

- High upfront costs , A fully outfitted commercial truck in New York can cost $75,000 to $200,000 before your first customer places an order.

- Permitting and commissary fees , NYC requires mobile food vendors to operate from a licensed commissary kitchen, adding a recurring overhead expense.

- Event and festival deposits , Landing a prime spot at Smorgasburg or the NYC Summer Streets program often requires advance payment months before the event.

Traditional banks often shy away from food trucks because they lack the commercial real estate collateral that secures most small business loans. That’s exactly where alternative small business funding steps in.

1. Merchant Cash Advance (MCA) , Best for Fast Access to Capital

A Merchant Cash Advance is the go-to funding solution for NYC food trucks that process credit and debit card sales. Rather than a traditional loan, an MCA provider advances you a lump sum of cash in exchange for a fixed percentage of your future card receipts , repaid automatically each day until the balance is settled.

How It Works for Food Trucks

If your food truck processes $25,000/month in card sales, you might qualify for a $30,000–$60,000 advance. The funder deducts a small daily percentage (called a “holdback rate,” typically 8–15%) from your card transactions until the advance plus a factor fee is repaid. On busy festival weekends, you repay more; on slow winter days, you repay less.

The payment scales with your revenue , making it one of the most cash-flow-friendly structures in alternative lending.

Who Qualifies

- At least 3–6 months in business

- Minimum $8,000–$10,000/month in card sales

- Credit scores as low as 500 accepted

- No collateral required

At Lending Valley, food truck owners can be approved and funded the same day , often within 2–4 hours of submitting an application. Learn more about our Merchant Cash Advance program or bad-credit business loan options if your score is a concern.

2. Equipment Financing , Best for Purchasing or Upgrading Your Truck

Need to buy a new food truck, upgrade your cooking rig, or add a second unit to your fleet? Equipment financing is purpose-built for exactly this. The equipment itself serves as collateral, which means lenders take on less risk , and you can often qualify with a lower credit score and receive competitive rates.

Key Advantages

- Finance up to 100% of the equipment cost (truck, generator, refrigeration, POS systems)

- Repayment terms up to 5–7 years, reducing monthly cash outflow

- Interest may be tax-deductible under Section 179

- You own the equipment outright when the loan is repaid

NYC-Specific Considerations

In New York City, food truck builds must meet NYC Department of Health standards, which can add $10,000–$30,000 to a base truck build. Equipment financing can bundle the truck, build-out, and required health equipment (sneeze guards, ventilation) into a single loan , covering your total cost in one clean package.

3. Revenue-Based Working Capital Loans , Best for Seasonal Operators

If you operate primarily during warm-weather months , at NYC parks, rooftop events, or outdoor markets , a revenue-based working capital loan can bridge your seasonal gaps. Unlike a traditional bank loan with rigid monthly payments, revenue-based loans from alternative lenders like Lending Valley are tied to your actual monthly deposits.

How Repayment Works

Instead of a fixed monthly payment, the lender reviews your average monthly bank deposits to establish a daily or weekly ACH repayment amount. If you pull in $40,000 in October and $12,000 in January, the loan accommodates that reality. This flexibility makes working capital loans a strong fit for caterers with event-driven income and food trucks that park only seasonally.

Explore small business loan options or speak with a funding advisor at Lending Valley to find the right structure for your revenue profile.

According to the Federal Reserve’s Small Business Credit Survey, 43% of small businesses applied for financing to cover operating expenses and cash flow gaps , the most common reason cited , making working capital loans one of the highest-demand products in the alternative lending space.

4. SBA Microloans and 7(a) Loans , Best for Lower Rates and Longer Terms

The U.S. Small Business Administration (SBA) offers two programs worth knowing about if you’re a food truck owner or caterer willing to navigate a longer approval process in exchange for better rates.

SBA Microloan Program

SBA microloans provide up to $50,000 through approved nonprofit intermediary lenders. Interest rates typically range from 8% to 13%, with repayment terms up to six years. This is ideal for first-time food truck operators who need startup capital for equipment, permits, or initial inventory. Credit requirements are more flexible than conventional bank loans, and many NYC-area microlenders offer free technical assistance alongside the loan.

SBA 7(a) Loan Program

For established food truck businesses seeking larger sums , up to $5 million , the SBA 7(a) loan offers competitive rates (Prime + 2.25–4.75%) and repayment terms up to 10 years. The trade-off is time: approval can take 4–8 weeks, extensive documentation is required, and not all food trucks will meet the underwriting standards. If you need capital in days rather than weeks, an MCA or working capital loan is a more practical path.

Ready to Get Your Food Truck Funded?

Apply in minutes. Lending Valley approves NYC food trucks and caterers with revenue as low as $8,000/month , no collateral, no tax returns, no perfect credit required.

5. Invoice Factoring , Best for Catering Companies with Outstanding Invoices

Catering companies that bill corporate clients, wedding venues, or government agencies often wait 30, 60, or even 90 days for payment , even after a successful event. Invoice factoring solves this cash flow problem by letting you sell your outstanding invoices to a factoring company at a small discount in exchange for immediate cash.

How It Works

You submit your unpaid invoices to the factoring company. They advance you 80–90% of the invoice value , typically within 24–48 hours. Once your client pays the invoice, the factoring company releases the remaining balance minus their fee (typically 1–5% of the invoice value). There’s no debt on your balance sheet and no monthly repayment schedule.

Ideal Use Case

A Brooklyn-based catering company books a $40,000 corporate event in February for delivery in April , but operating costs (staff, ingredients, rentals) hit in March. By factoring a prior $25,000 invoice, they bridge the gap without borrowing traditionally. The factoring fee might be $750–$1,250 , a fraction of what a business disruption could cost.

Side-by-Side Funding Comparison for NYC Food Trucks & Caterers

Here’s how the five options stack up across the factors that matter most to mobile food operators:

| Funding Type | Funding Amount | Speed to Fund | Credit Req. | Collateral | Best For |

|---|---|---|---|---|---|

| Merchant Cash Advance | $5K – $500K | Same day – 24 hrs | 500+ FICO | None | Fast capital; card-heavy sales |

| Equipment Financing | $10K – $500K | 2–5 business days | 600+ preferred | Equipment itself | Truck purchase or upgrade |

| Working Capital Loan | $10K – $250K | 24–48 hours | 550+ FICO | None | Seasonal gaps; operating costs |

| SBA Microloan | Up to $50K | 2–8 weeks | Flexible | Sometimes | Startups; low-rate financing |

| SBA 7(a) Loan | Up to $5M | 4–8 weeks | 680+ preferred | Often required | Large expansion; long terms |

| Invoice Factoring | 80–90% of invoices | 24–48 hours | Client credit matters | Invoices | Caterers; B2B cash flow gaps |

How to Apply for Food Truck Financing in NYC

At Lending Valley, the application process for food truck and catering businesses is designed to be as frictionless as possible. Here’s what to expect:

- Submit your application online , Takes about 5–10 minutes. Basic business info, estimated monthly revenue, and intended use of funds.

- Provide 3–6 months of bank statements , No tax returns, no P&L statements required for most products. We underwrite based on your actual cash flow.

- Receive your offer , A dedicated funding advisor reviews your file and presents a personalized offer, often within the same business day.

- Accept and get funded , Once you accept your offer, funds are wired directly to your business bank account , as fast as the same business day for MCAs and working capital products.

If you’re not sure which product fits your situation, our funding specialists can walk you through your options in a no-pressure consultation. There’s no obligation to apply, and checking your options won’t affect your credit score.

Frequently Asked Questions: Food Truck Financing NYC

How much can a food truck owner borrow in NYC?

Depending on the funding type, NYC food truck owners can borrow anywhere from $5,000 (SBA microloan) to $500,000 or more (equipment financing or MCA). The right amount depends on your monthly revenue, time in business, and intended use of funds. Most alternative lenders base approval primarily on your cash flow , not your credit score.

What is the easiest type of funding for a NYC food truck?

A Merchant Cash Advance (MCA) is typically the fastest and easiest option for food trucks that process credit and debit card sales. Approval can happen within hours, and funding is often deposited the same day or next business day , with minimal paperwork and no collateral required.

Can I get food truck financing in NYC with bad credit?

Yes. Alternative lenders like Lending Valley approve food truck and catering businesses with credit scores as low as 500. Instead of focusing on your FICO score, they look at your monthly revenue, bank statements, and time in business. SBA microloans also have flexible credit requirements through certain nonprofit lenders. See our bad-credit business loan options for more details.

How quickly can a NYC food truck get funded?

With an MCA or revenue-based loan through an alternative lender, you can receive funding in as little as 24 hours of applying. SBA loans typically take 2–8 weeks due to documentation and underwriting requirements. Equipment financing timelines fall somewhere in between, often 2–5 business days.

Do catering businesses qualify for invoice factoring?

Yes , catering companies that invoice corporate clients, event venues, or government agencies are strong candidates for invoice factoring. The factoring company advances you up to 80–90% of your outstanding invoice value, giving you immediate working capital without waiting 30, 60, or 90 days for payment.

The Bottom Line

Running a food truck or catering operation in New York City is a real business , and it deserves real capital solutions. Whether you need same-day cash to cover a busted refrigeration unit, equipment financing to launch your second truck, or invoice factoring to stop waiting on slow corporate clients, there is a product designed specifically for how your business operates.

The biggest mistake mobile food operators make is waiting until they’re in a cash crisis to explore their options. The best time to understand your funding choices is before you need them , so when opportunity (or an emergency) strikes, you’re ready to move fast.

Lending Valley has helped hundreds of New York food entrepreneurs access fast, flexible funding with minimal paperwork and no runaround. If you’re ready to explore your options, apply today , it takes less than 10 minutes, and you’ll have a decision the same day.

Apply for Food Truck Financing Today

No collateral. No tax returns. Credit scores from 500 accepted. Get a same-day decision from Lending Valley’s NYC funding experts.

About the Author: Chad Otar is the founder and CEO of Lending Valley, a New York-based alternative business funding company. With over a decade of experience in small business finance, Chad has helped thousands of entrepreneurs

Food Truck Financing NYC: 5 Funding Options to Keep Your Business Rolling in 2026