Knowing how to get a microloan for small business, and which program fits your situation, is what separates the business owners who get funded from the ones who keep getting rejected. This guide walks you through every step.

Table of Contents

What Is a Microloan?

A microloan is a small business loan, typically between $500 and $50,000, designed for entrepreneurs who need a modest amount of capital but can’t access traditional bank financing. The term “microloan” covers a range of products, from government-backed SBA loans to community development financial institution (CDFI) loans to fast-approval alternative lending products.

Microloans fill a critical gap in small business financing. Banks typically won’t lend less than $100,000 because small loans aren’t worth the underwriting cost. That leaves startups, sole proprietors, side hustlers turning into full businesses, and small operators without a lot of collateral — in a funding desert. Microloans were created specifically to solve this problem.

Types of Microloan Programs Available in 2026

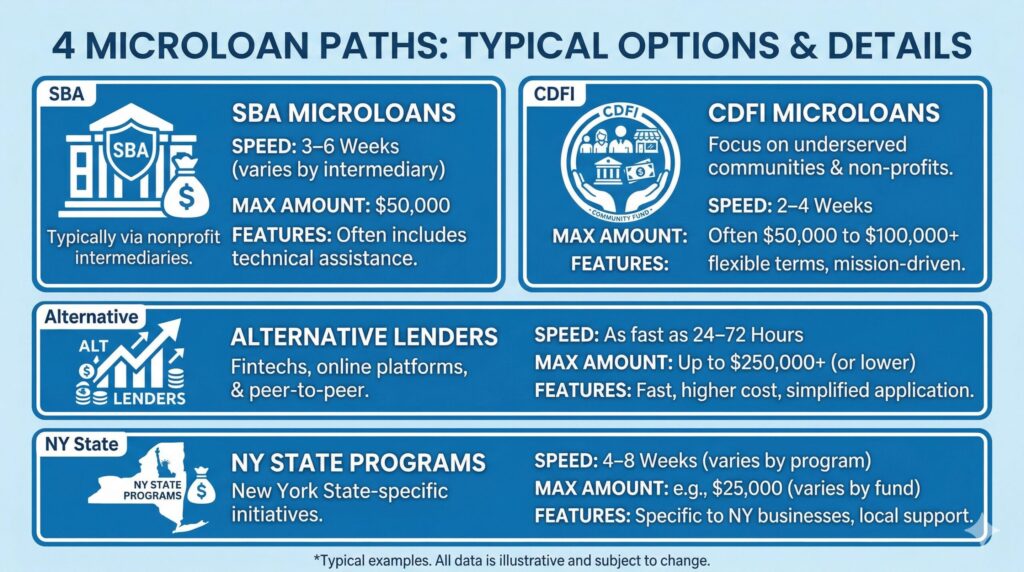

SBA Microloan Program

The U.S. Small Business Administration Microloan Program is the best-known microloan option in the country. Loans go up to $50,000 through a network of approved nonprofit intermediary lenders. Interest rates typically run 8–13%, and repayment terms extend up to seven years. Many SBA intermediaries also offer mentoring, training, and technical assistance, which can be as valuable as the capital itself.

CDFI (Community Development Financial Institution) Loans

CDFIs are mission-driven lenders, nonprofits, credit unions, and community loan funds, that serve low-income entrepreneurs and underserved markets. They often accept lower credit scores and require less documentation than banks. Interest rates are typically competitive with SBA rates, and many CDFIs offer loans as small as $500. New York State has a robust CDFI network with access to revolving loan funds with rates as low as 3–8%.

Alternative and Online Microlenders

Private alternative lenders and fintech companies offer microloan-sized funding, typically $5,000 to $50,000, with far faster approval timelines than SBA or CDFI programs. Think 24–48 hour funding instead of 2–4 weeks.

The tradeoff is cost: alternative products often carry higher factor rates or APRs. But for a business owner who needs capital now, not next month — this can absolutely be worth it. Lending Valley works with 50+ lenders to find you the best available rate across this entire category.

Nonprofit and State-Specific Programs

New York State runs several microloan-adjacent programs worth knowing about. The State Small Business Credit Initiative (SSBCI) has deployed more than $55 million to support small business lending statewide, including microloan and short-term loan programs under $250,000. The New York Forward Loan Fund offers working capital loans up to $150,000 at fixed rates between 8.25% and 11.25%.

Microloan Programs Compared: Side-by-Side

| Program Type | Max Amount | Rate Range | Approval Time | Min. Credit Score | Best For |

|---|---|---|---|---|---|

| SBA Microloan | $50,000 | 8%–13% | 2–4 weeks | 575–620+ | Startups, low-income areas, mentoring |

| CDFI Loan | $25,000–$100K | 3%–10% | 5–15 business days | 500–580+ | Underserved / minority-owned businesses |

| Alternative / Online Lender | $5K–$50K | 14%–40%+ APR | 24–48 hours | 500+ | Speed, bad credit, low documentation |

| NY State Programs (SSBCI / Forward) | Up to $150,000 | 8.25%–11.25% | 2–6 weeks | 620+ | NY businesses needing affordable rates |

| Merchant Cash Advance (MCA) | $5K–$500K | Factor rate 1.15–1.5 | Same day – 48 hrs | 500+ | Revenue-based, no fixed payments |

How to Qualify for a Microloan

Qualification requirements vary by program, but here’s what the vast majority of microloan lenders look at:

Credit Score

Microloans are specifically designed to be accessible to borrowers who don’t have perfect credit. SBA microloan intermediaries will often work with scores as low as 575. Many CDFI and nonprofit lenders focus more on character and business viability than raw scores.

Alternative lenders typically accept scores from 500 and up. The bottom line: don’t assume your credit score disqualifies you. Apply and let the lender make that determination. Our bad credit business loan options are designed exactly for this situation.

Time in Business

SBA microloan programs and nonprofit CDFIs are startup-friendly, some will fund businesses with zero operating history if you have a credible business plan. Alternative lenders typically want at least 3–6 months in business. State programs often require 6–12 months. If you’re brand new, the SBA route or a CDFI are your best options.

Revenue and Cash Flow

Lenders want to see that you can repay. For established businesses, 3–6 months of bank statements showing consistent revenue is usually enough. For startups, a detailed financial projection and business plan can substitute for revenue history with many microloan programs. Alternative lenders will look primarily at monthly bank deposits, a minimum of $5,000–$10,000 per month is typical.

Business Plan (For SBA and Nonprofit Programs)

SBA intermediaries and CDFIs often require a business plan, a written description of your business, target market, competitive advantage, and financial projections. This doesn’t need to be an MBA thesis. A clear, honest 2–3 page plan showing you’ve thought through your business can be enough to satisfy most microloan programs.

Collateral

Most microloans don’t require significant collateral. The SBA Microloan Program notes that intermediaries “may require collateral” — but this is typically minimal compared to traditional loans. Alternative lenders and MCAs are generally fully unsecured, with no collateral required at all. A personal guarantee is common across most microloan programs.

Step-by-Step: How to Apply for a Microloan

Step 1: Assess how much you actually need.

Step 2: Check your credit score and clean it up.

Step 3: Choose the right program for your timeline.

Step 4: Gather your documents.

Step 5: Submit your application.

Step 6: Review your offers carefully.

Step 7: Get funded and track your ROI.

Ready to Apply for a Microloan?

One 2-minute application. 50+ lenders. Lending Valley finds the best fit for your business, from same-day MCA to low-rate SBA options.

What Can You Use a Microloan For?

Microloans are flexible, but lenders do care how you use the money. Here’s what’s typically allowed, and what’s not:

Common Approved Uses

Working capital (covering payroll, rent, utilities), purchasing inventory or supplies, buying equipment or tools, furniture and fixtures, marketing and advertising campaigns, hiring and training employees, website development and digital tools, and covering short-term cash flow gaps.

Restricted Uses (SBA Program)

SBA microloans cannot be used to pay off existing debt or purchase real estate. If either of those is your goal, you’ll need a different product — a 7(a) loan for debt consolidation, or a commercial real estate loan for property.

Most alternative microlenders are less restrictive, as long as the funds are used for legitimate business purposes, they typically don’t dictate how you allocate the capital.

When a Microloan Isn’t the Right Fit

Microloans are a great tool, but they’re not always the best answer. Here’s when to consider something else:

You need more than $50,000 fast. A short-term business loan or merchant cash advance can deliver $50K–$500K in 24–48 hours, with minimal documentation. SBA 7(a) loans can go up to $5 million for qualified businesses.

You need revolving access to capital. A business line of credit is more flexible than a one-time microloan — draw what you need, repay, and draw again. It’s ideal for businesses with unpredictable or recurring capital needs.

You have unpaid invoices slowing you down. Invoice factoring converts outstanding invoices into immediate cash — typically 80–90% of the invoice value, without taking on new debt at all.

Your equipment is the bottleneck. If you need to buy or lease equipment specifically, equipment financing uses the equipment itself as collateral, often unlocking better rates than unsecured microloan products.

Frequently Asked Questions

What credit score do I need to get a microloan?

There’s no universal minimum. SBA microloan intermediaries often work with scores from 575–620. CDFI lenders may go lower, focusing more on character and business viability. Alternative lenders typically accept 500+. Don’t let an imperfect score stop you from applying, see bad credit business loan options for more guidance.

How long does it take to get a microloan?

SBA and CDFI programs typically take 2–4 weeks. State programs can take 2–6 weeks. Alternative online lenders can fund in 24–48 hours. If you need same-day funding, an MCA or short-term loan is the fastest route — see Lending Valley’s same-day funding options.

Can a startup get a microloan?

Yes, the SBA Microloan Program was specifically designed for startups and early-stage businesses. Many CDFI programs also fund pre-revenue businesses with strong business plans. Alternative lenders generally require 3–6 months of operating history.

What can I use a microloan for?

Working capital, inventory, equipment, supplies, marketing, hiring, and technology are all approved uses. SBA microloans cannot be used for real estate or debt payoff. Most alternative lenders place no restrictions on use beyond basic business purposes.

What is the maximum amount for a microloan?

The SBA caps its Microloan Program at $50,000. Other microlenders offer up to $100,000. If you need more, explore small business loans up to $500,000 or SBA 7(a) loans up to $5 million.

The Bottom Line

Getting a microloan for your small business in 2026 is more achievable than most entrepreneurs realize. The SBA Microloan Program, CDFI lenders, and alternative fintech lenders have collectively removed most of the traditional barriers, credit score requirements, collateral demands, and revenue minimums are all more flexible than what you’d face at a bank.

The key is matching the right program to your specific situation. If you can wait a few weeks and want the lowest cost of capital, pursue an SBA or CDFI microloan. If you need money in 24–48 hours, alternative lenders can deliver. And if your needs are bigger or more complex, Lending Valley can walk you through the full range of options — from a $10,000 MCA to a $5 million SBA loan.

Ready to find out what you qualify for? Apply in 2 minutes — no obligation, no impact to your credit.